Our entire team is devoted to our commitment of providing only exceptional service, from our sales team, to our operations professionals, to secondary marketing and to our management team.

Absolute Mortgage & Lending is a dba of AML Funding, LLC. At Absolute Mortgage & Lending, we all share one vision and practice our core values. We strive to provide excellent service to our clients and partners and hold great value in being the mortgage lender our clients turn to.

We believe that 95% of mortgage loan processing problems are unnecessary and can be totally eliminated. It's what drives us to share our knowledge and resources. We know from experience that delays caused by errors, missing information and a mountain of underwriting conditions can quickly become a thing of the past. This belief inspired us to design a user-friendly, online course that makes complex mortgage loan processing principles easy to understand.

Partner Perks

Access to sales strategies and coaching

Extensive loan program options

Pre underwriting, processing + 20 yrs of origination experience

Weekend availability

Marketing and community outreach support

7 touch follow up process for leads

Face to Face joint client agent consultation

Preferred Lender Incentives with New Construction Relationships

Property marketing and exposure

Assistance with marketing videos and photos for listings

Fast closings

Completive rates and closing costs for our clients

Weekly communication with all parties of the transaction

Client Services

Complete Client Interview

Face to Face Consultation with a personalized Plan of Action

Preapproval Letter vs Prequalification Letter with Automated underwriting findings

Weekly Follow up and weekend availability

Access to the Best Resources; Credit Repair, Insurance Agent, Rapid Rescore, Accounting and more.

12 hour Underwriting scenarios

Privacy Protection

20 day Closing

Competitive products, investors friendly programs including residential, commercial and hard money.

Same day approval

Ability to pre-underwriting a application

Detailed explanation on; Timeline of the Loan Process, my teams role, the Do’s and Don’ts, Current Market rates, Homestead application, Debt to income ratios, Bank vs Lender explanation, FHA vs Conventional explanation, Loan Level Price Adjustments, Closing costs, monthly payments and escrow accts.

What is a Conventional Loan?

By definition, a conventional loan is any mortgage that is not guaranteed or insured by the federal government. A conventional loan is generally referring to a mortgage loan that follows the guidelines of government sponsored enterprises (GSE’s) like Fannie Mae or Freddie Mac. Conventional loans may be either “conforming” and “non-conforming.” Conforming loans follow the terms and conditions set by Fannie Mae and Freddie Mac. Non-conforming loans don’t meet Fannie Mae or Freddie Mac guidelines, but they are also considered conventional.

Whether you’re buying a home or want or refinance your mortgage, a Conventional Loan might be right for you. If you’re unsure about your credit rating, or have concerns about a down payment, Conventional Mortgages can give you piece of mind with low-closing costs and flexible payment options.

What are the Conventional Loan Requirements?

To decide if you qualify for a Conventional Mortgage Loan, we will look at:

* Your income and your monthly expenses. Standard debt-to-income ratios are 28/36 for Conventional Loans. These ratios may be exceeded with compensating factors.

* Your credit history (this is important, but Conventional’s credit standards are flexible). A FICO score of 620 or above is very helpful in obtaining an approval.

* Your overall pattern rather than individual problems you may have had.

To be eligible for a Conventional mortgage, your monthly housing costs (mortgage principal and interest, property taxes and insurance) must meet a specified percentage of your gross monthly income (28% ratio). Your credit background will be fairly considered. At least a 620 FICO credit score is generally required to obtain a Conventional approval. You must also have enough income to pay your housing costs plus all additional monthly debt (36% ratio). These percentages may be exceeded with compensating factors.

What are the Conventional Down Payment Requirements?

Conventional Loans require the home buyer to invest at least 5% – 20% of the sales price in cash for the down payment and closing costs. If the sales price is $100,000 for example, the home buyer must invest at least $5,000 – $20,000.

What will my Interest Rate be?

The interest rate for your home loan will be determined by the type of loan program that you qualify for and your credit score

What types of property are eligible?

While Conventional Mortgage Guidelines allow you to purchase warrantable condos, planned unit developments, modular homes, manufactured homes, and 1-4 family residences. Conventional Loans can be used to finance primary residences, second homes and investment property.

Ready to get your loan process started? Click Here & Start Your Loan Application.

Can I get a Conventional Mortgage Loan after bankruptcy?

Criteria for Conventional loan approvals state that if you have been discharged from a Chapter 7 bankruptcy for four years or more, you are eligible to apply for a Conventional mortgage. If you have had a Chapter 13 bankruptcy, it must be documented that your credit reputation has been re-established for at least two years to be eligible for a Conventional Loan Application.

What kinds of loans do Conventional Programs Offer?

Fixed rate loans – Most Conventional Mortgages are fixed-rate mortgages. In a fixed rate mortgage, your interest rate stays the same for the entire loan period. With a fixed rate Conventional Mortgage, you always know exactly how much your monthly payment will be. Contact us for today’s Conventional mortgage rates.

Adjustable rate loans – With a conventional adjustable rate mortgage (ARM), the initial interest rate and monthly payments are low, but these may change during the life of the loan.

Ready to get your loan process started? Click Here & Start Your Loan Application.

Our Construction Loan Services

Building the custom home of your dreams means your future holds many wonder-filled possibilities. Finding the interim construction financing product that best fits your needs should not be one of those wonders.

At Absolute Mortgage & Lending, we always say, “Your Custom Home Deserves Custom Home Financing.”

Securing an interim construction loan with Absolute Mortgage & Lending gives you the peace of mind you desire, so you can focus on the more important aspects of your custom home build.

Why an Absolute Mortgage & Lending loan?

Our borrowers have found that we offer specialized construction loan products with unique terms that are not offered by most lenders. We make it easy for you to obtain a make-sense construction loan, and then transition that construction loan to a permanent mortgage after your custom home is complete.

The Absolute Mortgage & Lending loan advantage for borrowers:

· Minimal down payment options

· Cash lot equity counts as down payment

· Loans up to $1 MIL

· Credit score requirements that are much lower than standard commercial banks

· Owner-occupied and second-home financing with a single-family home custom-build

· In-house financing for interim and permanent mortgage loan

· Transparent, up-front underwriting on permanent loan

· Simultaneous close for lot purchase and interim construction financing

One loan Originator. One borrower. One team. One-stop shop.

Our focus is on providing outstanding customer care and the best mortgage product available for your unique situation. The Absolute Mortgage & Lending loan originators work one-on-one with you throughout the entire process, from loan application to closing the permanent mortgage. No need to juggle multiple loan originators and loan notes from multiple lenders. Absolute Mortgage & Lending is your one-stop shop for all your mortgage-lending needs.

Whether you’re looking to build your third custom home or wanting to build your first due to bidding wars and low home inventory, rest assured your decision to go with Absolute Mortgage & Lending is a smart choice.

Make-sense solutions for borrowers and builders alike.

Absolute Mortgage & Lending is a pioneering leader in the construction-to-permanent mortgage lending. We developed a highly customized construction lending division that provides maximum financing on interim construction loans in the State of Texas and other eligible regions. Absolute Mortgage & Lending underwrites and funds its own loans. There is no third-party underwriter to slow the process. Borrowers looking to build the custom home of their dreams are able to get their construction loan faster with the use of Absolute Mortgage & Lending’s lower down payment options and the expertise of our construction loan originators.

Builders and the local community benefit from the advantage, too. There is more profit in the builder’s pocket when the borrower secures a low down-payment construction loan at Absolute Mortgage & Lending.

Look at the benefits of a loan with Absolute Mortgage & Lending for the builder:

· No retainage hold back

· Flexible draw schedules

· Easy builder approval

· One loan originator, one relationship, one servicer from interim to permanent loan

· In-house financing for interim and permanent mortgage loan

· Transparent, up-front underwriting on permanent loan

· Simultaneous close for lot purchase and interim financing

· Quick turn time on interim closing, within 30 days of receiving final contract, plans, and specs

Ready to get your loan process started? Click Here & Start Your Loan Application.

Offering a variety of options for Commercial Real Estate Financing. Whether you are building, renovating, or purchasing we can customize a lending package to meet your needs.

Real Estate lending options:

* Construction

* Renovation

* Purchase

Every business needs a little extra cash from time to time. We have a wide variety of financing options to keep your business going and growing.

Offering:

* Fixed or Variable Rate

* Variable Terms

* Unsecured and Secured Options available

* Fast Approvals

Ready to get your loan process started? Click Here & Start Your Loan Application.

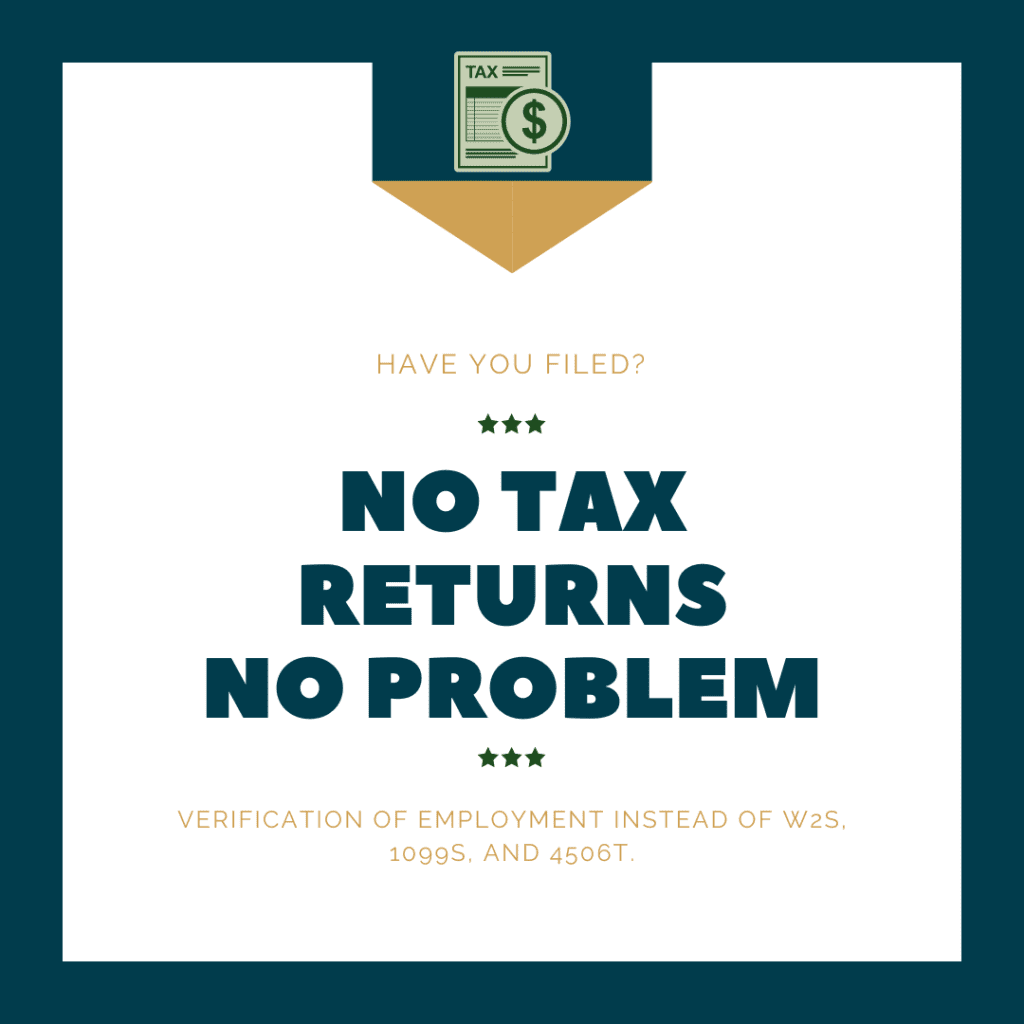

Although FHA loans typically require tax returns for income verification, there are situations where you may be eligible without them. If you are a wage earner and have yet to file income taxes but want to purchase a home using an FHA loan, this may apply to you. A Verification of Employment (VOE) will be required instead of tax returns. Below are what you would expect to process this type of mortgage application.

Program Highlights:

* No tax returns, no W2s, and no 4506T

* Must be employed for at least two years, preferably with the same employer or same line of business (all employment VOE)

* Business: google recognized, brick & mortar

* Non-arm’s length transaction

* Minimum Loan Amount of $50,000

* Current Pay stub Covering 30‐Days of Employment

Not Allowed:

* Family Employer

* Self‐Employed and Investment Income

* Down Payment Assistance Programs

* Departing Residence Income

Credit Minimums & DTI Allowed:

* 580+ FICO LTV UP TO 96.5% MAX DTI 55%

* 540 – 579 FICO LTV UP TO 90% MAX DTI 50%

Ready to get your loan process started? Click Here & Start Your Loan Application.

A jumbo loan is used to finance properties that exceed the allowed loan limits of a conventional conforming loan. The maximum amounts allowed for conforming loan changes annually and vary by county. The Federal Housing Finance Agency (FHFA) determines this mortgage loan amount.

Credit score

To qualify for a jumbo loan, lenders may require your FICO score to be higher than 680.

Debt-to-income ratio

Lenders will consider your debt-to-income ratio (DTI) to ensure you don’t become over-leveraged. PMI is not assessed on Jumbo loans.

Max Loan Amount is $3 Million.

Partnerships for loan sizes above 3 million can be considered in a case-by-case scenario.

Documentation

Be prepared to provide your complete tax returns, W-2s, and 1099s when applying, in addition to bank statements and information on any investment accounts to show credit and income health.

Appraisals

Some lenders may require a second home appraisal and use the average of the two estimates for the home value.

Ready to get your loan process started? Click Here & Start Your Loan Application.

Down payment assistance programs vary by state and county. Whether you’re a first-time homebuyer or looking to upgrade to a new property, these programs can offer valuable support to make homeownership more accessible and affordable.

We understand that everyone’s financial circumstances are unique, and our goal is to help you find the best down payment assistance program that fits your needs. By leveraging these programs, you can reduce the upfront costs associated with purchasing a home, making your dream of homeownership a reality.

We are committed to providing you with the resources and guidance to make informed decisions about your home-buying journey. Feel free to contact our licensed loan professionals for more details on the product offerings available in your area.

Below are the approved Down Payment Assistance Programs we offer at Absolute Mortgage & Lending.

Approved Programs: Arizona – Home Plus, California – CalHFA, Colorado – CHFA, Florida -FL Housing, Louisiana – LHC, Texas – DHAP, Texas State Affordable Housing Corporation – TSAHC

Ready to get your loan process started? Click Here & Start Your Loan Application.

There are a lot of reasons to ask for an FHA loan instead of taking a conventional or an expensive and riskier sub-prime mortgage loan. FHA has many advantages and benefits that other loans do not cover.

Easier to Qualify

FHA insures your mortgage and we are more willing to give you a loan with lower qualifying requirements which makes it easier for you as a buyer to qualify.

Costs Less

FHA loans have competitive interest rates because the loans are insured by the Federal Government. Always compare an FHA loan with other loan types.

Ready to get your loan process started? Click Here & Start Your Loan Application.

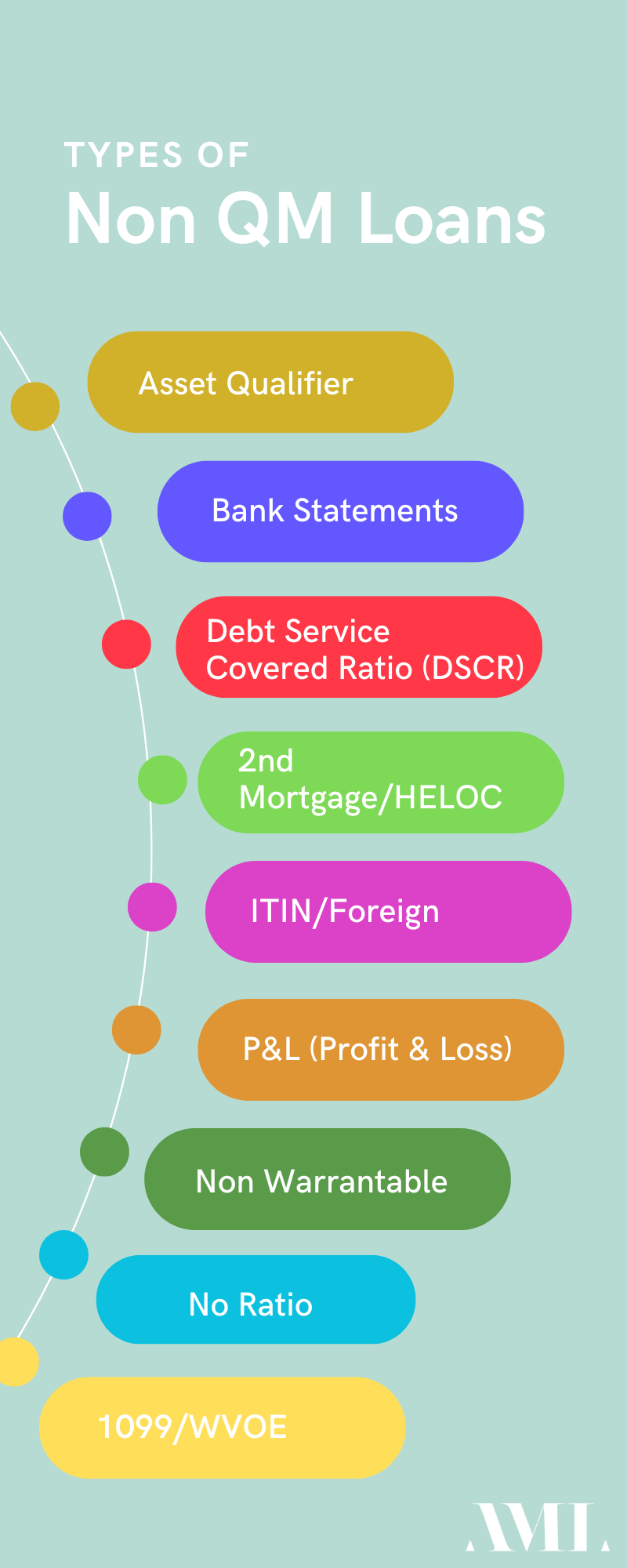

Nonqualified mortgages (non-QM) are alternative mortgage loan programs designed to help borrowers who can’t qualify using standard document programs. Government and conventional loans have set agency mortgage guidelines, which may disqualify many borrowers. For example, if you are self-employed or need all the necessary documentation to qualify for a traditional mortgage, you should look at nonqualified mortgages.

Without Non-QM loans, certain people could not purchase their homes. These loans are not backed by any government agency and are considered portfolio loans.

NON-QM Pros & Cons

PROS:

* Same Application as a traditional mortgage

* Lenient Guidelines requiring less proof of income and docs

* Products available for foreign national

* Investors are not limited to the number of financed doors they own

CONS:

* Interest Rates and fees may be higher

* NON-QM loans can be challenging to find

* Down Payment requirements may be higher

* Require higher credit scores

Who Benefits from Non-QM Loans

The following types of borrowers benefit:

* Investors who are CAPPED at the allowed number of doors financed

* Mortgage Borrowers who are self-employed and do not meet the

debt-to-income ratio requirements due to the business expenses

* Homebuyers with a prior bankruptcy and/or foreclosure who have

reestablished themselves but did not meet the minimum waiting

period requirements after bankruptcy and/or a housing event

* Homebuyers who have late mortgage payments in the last 12 months on their previous mortgage

* Retirees, self-employed, entrepreneurs, and wealthy individuals who

have assets but no traditional income and/or regular job

* High-end homebuyers who cannot qualify for traditional jumbo loans

Ready to get your loan process started? Click Here & Start Your Loan Application.

Are you ready to remodel, update or repair your home? But not sure how to fund your project? Let us help!

We have several loan programs to help you remodel, update or repair your home with one simple loan, no need for a 2nd mortgage, and no need to save up the cash. This is a one-time renovation refinance loan (purchase available too). We can accommodate all types of repairs and upgrades from a roof replacement to an extensive addition to your home’s square footage.

Ready to get your loan process started? Click Here & Start Your Loan Application.

The purpose of this program is primarily used to help low-income individuals or households purchase homes in rural areas.

USDA Rural Housing Program offers the following important features:

* 100% financing available

* 6% seller concessions allowed

* No maximum loan limits

* 30-year fixed-rate mortgages

* Must be in non-metropolitan areas

* Single-family/owner-occupied homes

If the appraised value is above the sales price you can use the difference for concessions, repairs, et

The USDA Rural Housing program provides low and moderate-income rural residents with better access to affordable housing financing options with little or no down payment or out-of-pocket costs. Borrowers may obtain a loan to purchase a new or existing home that is located in a designated rural area. Population of 10,000 or less; population of 20,000 or less if located outside a metropolitan statistical area. Eligibility: Borrower must lack sufficient resources to obtain conventional financing.

Occupancy: Primary

Loan Term 30-year fixed only. Purchase and Rate/Term Refinance. Income and geographic limits apply. Loan amount based on the lesser of the following: current conforming conventional loan limit, excluding the guarantee fee; 102.75% of the appraised value. Includes the guarantee fee.

The appraisal determines the maximum loan amount. (Note – guarantee fee changed from 2.75% to 1.00%, annual fee changed from 0.50% to 0.35% in Oct. 2016).

Ready to get your loan process started? Click Here & Start Your Loan Application.

VA guaranteed loans are made to eligible veterans for the purchase of a home which must be for their own personal occupancy. With a loan approval, VA will guarantee a portion of the loan to the mortgage lender.

This guarantee protects the lender against loss up to the amount guaranteed and allows a veteran to obtain favorable financing terms. A veteran still has to be qualified for their income and credit for the asking price of a purchase. 100% financing is subject to Veteran’s eligibility.

VA Loans offer the following important features:

* Equal opportunity for all qualified veterans to obtain a VA loan

* No down payment (unless required by the lender or the purchase price is more than the reasonable value of the property).

* Buyer informed of reasonable value.

* Negotiable interest rate.

* Ability to finance the VA funding fee (plus reduced funding fees with a down payment of at least 5% and exemption for veterans receiving VA compensation).

* Closing costs are comparable with other financing types (and may be lower).

* No mortgage insurance premiums.

* An assumable mortgage.

* Right to repay without penalty. VA assistance to veteran borrowers in default due to temporary financial difficulty.

Ready to get your loan process started? Click Here & Start Your Loan Application.

What is a 7(a) loan?

The 7(a) Loan Program, SBA’s most common loan program, includes financial help for small businesses with special requirements. This is the best option when real estate is part of a business purchase, but it can also be used for:

* Short and long-term working capital

* Refinance current business debt

* Purchase furniture, fixtures, and supplies

Key eligibility factors are based on what the business does to receive its income, its credit history, and where the business operates.

* Land, streets, utilities, parking lots, and landscaping

* Existing facilities

* Minimum down payment requirements as low as 10%

* Loan sizes $350,000-10,000,000

Types of buildings allowed and must be owner-occupied by the business, no landlords collecting rents) ex: Auto mechanics, hotels, RV Parks, medical practice, restaurants, etc.

Types of businesses allowed: No nonprofits, No investment property, No investors, No house flippers, No developers, No illegal businesses, No casinos. Must be a small business

What is an Express SBA loan?

Loan Amount up to 350K, Purpose is to be used for revolving lines of credit. Fast turnaround.

Ready to get your loan process started? Click Here & Start Your Loan Application.

Adding up your Qualified total deposits from Personal and Business Bank statements may be used as an alternative to tax returns to document a self-employed borrower’s to represent income.

Product Features

* Max DTI 50%

* No 4506-C or tax returns required

* Can use personal or business bank statements for qualifying

* 100% gift funds allowed on Primary and 2nd Home

* Non-QM waiting periods on negative credit events

* P & I reserve on the subject property only

* At least one of the borrowers must be self-employed for at least 2 years (25% or greater ownership) to qualify for this program.

** Primary and Second Home Properties Only! Only 1-unit properties are allowed on Second Home transactions.

Ready to get your loan process started? Click Here & Start Your Loan Application.

A Little More About Me

Juan Luis exudes positivity, enthusiasm, and a spirit of excellence in every sector he engages with. His ten years of engineering experience, preceding his real estate career, have significantly honed his attention to detail and forward-thinking abilities—skills that are invaluable in today's dynamic real estate market.

A native Houstonian, Juan's love for his city and its people is deep-rooted. Since 2008 years, his full immersion in real estate has positioned him as a valuable asset to his clients. As the broker and owner of MRG Realty, a beloved, family-oriented local brokerage, Juan and his team are committed to facilitating real estate transactions, whether it’s buying, selling, or investing.

In 2020, Juan expanded his expertise by becoming a mortgage loan officer. This role has enabled him to guide clients seamlessly through the interconnected processes of real estate transactions. Additionally, as a real estate investor, Juan appreciates the significance of non-traditional financing, a service he offers through Absolute Mortgage & Lending.

Outside of his professional realm, Juan is passionate about healthy living. He finds joy in jogging, hiking, working out, mountain biking, and watching live sports. He also enjoys fine dining, salsa dancing, comedic films, and most importantly, creating lasting memories with family and friends—who he also considers his peers at the office.

Juan Luis Macedo | Home Loan Originator | NMLS # 1866542

JuanLuis@AbsoluteML.com | D: 281-701-9303 | 2825 Wilcrest Drive Suite 150 Houston TX 77042

Absolute Mortgage & Lending | www.ezhomecredit.com |Co. NMLS # 1910591

NMLS Consumer Access | Texas Complaint Recovery Notice

AFFORDABILITY CALCULATOR

Quite affordable.